Why I Will Never Do Business With Amazon Again

Why Amazon Has No Profits

(I besides did a podcast with Ben Horowitz discussing these themes: see here )

Amazon has a tendency to polarize people. On i hand, there is the ruthless, relentless, ferociously efficient company that's building the Sears Roebuck of the 21st Century. Only on the other, at that place is the fact that nearly xx years after information technology was launched, information technology has yet to written report a meaningful profit. This chart captures the contradiction pretty well - massive revenue growth, no profits, or so it would seem. But really, neither of these lines gives you lot a practiced sense of what'southward actually going on.

Amazon discloses revenue in iii segments - Media, Electronics & General Merchandise ('EGM') and 'Other', which is generally AWS. Equally this chart shows, these look very unlike (this and virtually of the following ones employ 'TTM' - trailing 12 months, which smooths out the seasonal fluctuations and makes it easier to see the underlying trends). The media business is nonetheless growing, but information technology's the full general merchandise that has powered the explosion in revenue in the past few years. Meanwhile, the 'Other' line is growing but is yet much smaller.

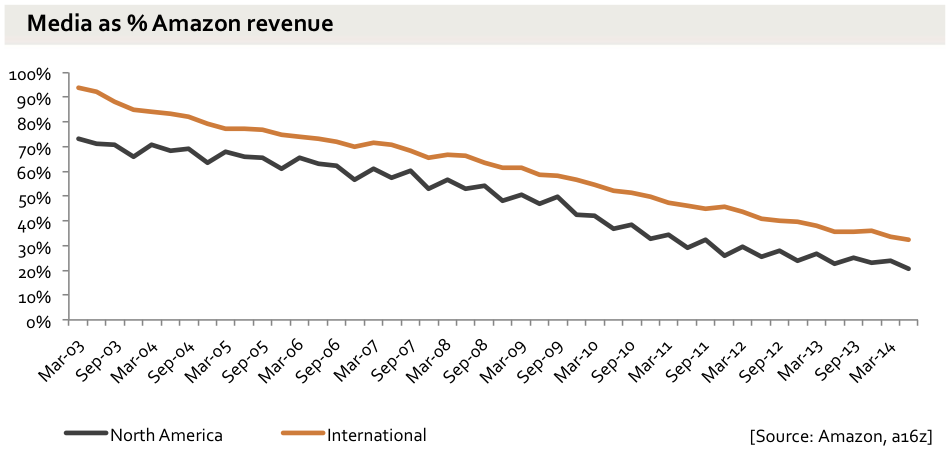

Splitting out the detail, we can see this trend both in North America (NA) and internationally...

Though the takeoff is especially strong in the The states.

Media overall was only 25% of Amazon's revenue last quarter, and 20% of Due north America.

And if we go back to 'Other' and zoom in, the growth is pretty dramatic there too.

It seems pretty likely that these businesses, selling very dissimilar products bought with different bargaining positions to different people with unlike aircraft costs, have different margin potential.

This still doesn't really requite an authentic picture, though. Amazon is in fact organized not only in these segments, but in dozens and dozens of split up teams, each with their own internal P&L and a high degree of autonomy. So, say, shoes in Germany, electronics in French republic or makeup in the USA are all dissimilar teams. Each of these businesses, incidentally, sets its own prices. Meanwhile, all of these businesses are at different stages of maturity. Some are relatively onetime, and well established, and growing slower, and are profitable. Others are new startups building their business and losing money as they do so, like any other new business concern. Some are very profitable, and some sell at toll or at every bit loss-leaders to drive traffic and loyalty to the site. Books are a good example. There'southward a widespread perception that Amazon sells books at a loss, just the average sales toll actually seems to be very close to physical retailers - it discounts some books, just not all, and despite all the statement in the Bureau lawsuits, quite how many and how much is (deliberately) as articulate every bit mud.

Amazon is a bundle.

The clearest expression of this is Prime, in which (amidst other things) entertainment content is included at a high fixed price to Amazon (buying the rights) only no marginal cost beyond bandwidth, equally a way to enhance the entreatment of beingness a Prime number 'member'. Prime membership in turn draws people to switch more than and more of their online and offline spending to Amazon. Trying to await at the profitability of the video solitary misses the point.

And then there are the tertiary party sales. Simply as AWS is a platform both for Amazon'south ain internal technologies and for thousands of startups, then too the logistics and commerce infrastructure themselves are a platform for lots and lots of different Amazon businesses, and also for lots of other companies selling concrete products through Amazon'southward site. Third political party sales of products through Amazon'south ain platform are at present 40% of unit sales, and the fees charged to these vendors are now twenty% of Amazon'due south revenue.

This means, in passing, that for close to half of the units sold on Amazon.com, Amazon does not set the price, it just takes a margin. This alone should point to the weakness of the idea that Amazon's growth is based on selling at toll or at a loss.

The tricky matter about these tertiary party ('3P') sales is that Amazon just recognizes revenue from the services it provides to those companies, not the value of the goods sold. So if you buy a pair of shoes on Amazon from a third party, Amazon might collect payment through your Amazon business relationship and ship them from its warehouse using its shipping partners - but simply show the shipping and payment fees it charged to the shoe vendor as revenue. It does non disclose the gross revenue ('GMV'). Given that (as it does disclose) tertiary party sales tend to have a higher unit value, this ways that the total value of goods that pass though Amazon with Amazon taking a percent is possibly double the acquirement that Amazon actually reports. So, the revenue line is non actually telling y'all what'south going on, and this is likewise one reason why gross margin is pretty misleading too. Gross profit has risen from 22.iv% in 2011 to 27.two% in 2013, just this does not really reflect a change in consumer pricing and margins thereof, but rather this modify in mix.

And so, we accept dozens of separate businesses within Amazon, and over two 1000000 third party seller accounts, all sitting on top of the Amazon fulfillment and commerce platform. Some of them are mature and profitable, and some are not. And someone at Amazon has the job of making sure that each quarter, this nets out to as close to naught as possible, at least equally far equally net income goes. That is, the trouble with cyberspace income is that all information technology tells us is that every quarter, Amazon spends whatever's left over to get the number to nada or thereabouts. There's really no other fashion to attain that sort of consistency.

If you listen closely, Amazon itself tells us this. The paradigm below comes direct from Amazon - originally information technology was a napkin sketch by Jeff Bezos. Note that there'due south no pointer pointing outwards labeled 'take profits.' This is a closed loop.

(Source: Amazon)

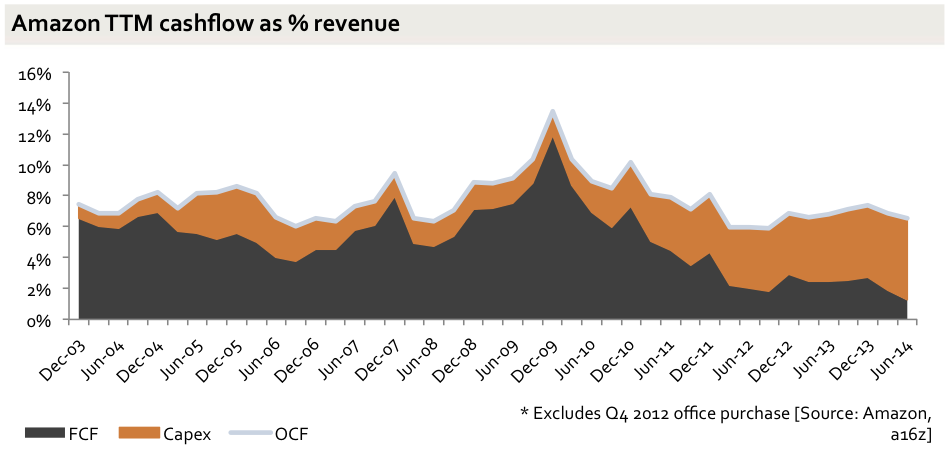

In any case, profits equally reported in the net income line are a pretty bad fashion to endeavor to understand a business similar this - actual cash menstruation is better. As the maxim goes, profit is stance but cash is a fact, and Amazon itself talks near cash period, non net income (Enron, for obvious and nefarious reasons, was the other mode around). Amazon focuses very much on gratuitous cash flow (FCF), just it's very useful to look also at operating cash flow (OCF), which is simply what yous get adding back majuscule expenditure ('capex'). In effect, OCF is the bulk of running the business before the costs of the infrastructure, Thousand&A and financing costs. This shows you the outcome of selling at low prices. Equally we tin see hither, Amazon's OCF margin has been very roughly stable for a decade, just the FCF has fallen, due to radically increased capex.

In absolute terms, you can therefore see a concern that is spinning out rapidly growing amounts of operating cash flow - over $5bn in the terminal 12 months - and ploughing it back into the business as capex.

Charting this as lines rather than areas shows simply how consistent the growth in capex has been.

Ane might propose that in a logistics business with rapid revenue growth, rapid capex growth is but natural, and i should expect at the ratio of capex to sales past itself. Simply in fact, the increase here is even more than dramatic. Starting in 2009, Amazon began spending far more on capex for every dollar that comes in the door, and there's no sign of the rate of increment slowing down.

If Amazon had held capex/sales at the same ratio from 2009, earlier it exploded, then FCF would look like this. That difference adds up to just over $3bn of cash in the last 12 months. That is, if Amazon was spending the same on capex per dollar of acquirement as it was in 2009, it would have kept $3bn more than in cash in the last 12 months.

So where'due south all the actress capex going? And, crucially, does it need to stay at these new, higher levels to back up Amazon'south business, or can it come back down in the future?

It's pretty credible that the money is going into more than fulfillment capacity (warehouses, to put it crudely) and to AWS. Hence, this chart shows an enormous increase in Amazon's physical infrastructure, every bit measured in square feet - this is most all fulfillment rather than data centers, though Amazon no longer gives a split.

Pulling apart precisely where the coin's going, though, is a little fiddlier. The increase is driven by some combination of four things:

-

More chapters for more products, including 3P products

-

Proximity - as Amazon builds warehouses closer to customers, the shipping time goes downwards and so too does the shipping cost, a further flywheel upshot for Prime

-

AWS

-

More expensive warehouses - that is, the existing business concern is becoming more than expensive to run

The first two of these are straightforward investment in the future, oft delivering higher future margins. AWS is a black box and a much debated puzzle, but information technology is likewise pretty much the definition of a new business organization that requires investment to abound. The real carry instance here would be the final point - that the existing business is becoming more capex-intensive - that more dollars of capex are needed for every dollar of current revenue.

Just to brand life harder for those looking to understand Amazon's financials, the warehouse expansion, capex expansion and AWS build-out all started at roughly the same time, and at that same moment Amazon inverse the manner it reports to brand it very difficult to pick them apart. Until 2010 information technology separate both holding and asset value between fulfillment and data centers, simply at that point it stopped, probably not by co-incidence (in 2010 Amazon had just 775k square feet for information centers and client service combined). In the concurrently, in that location are various metrics (capex per square foot, for instance) that would show a shift of spending from cheap warehouse to expensive information centers - but they would too show a shift from maintaining existing warehouses to edifice new ones. And then at that place is no direct, piece of cake style we tin can see the split.

We can still, though, go a something of a sense of the key warehouse question - has the business concern got more expensive to run? Information technology looks similar the reply is no. First, the third party sales do not seem to be the issue: ratio of 3P units has not gone up at anything like the fashion the capex/sales has over the same menstruation (here'south that nautical chart once again).

Neither is there any sign of a shift in the fulfillment costs over the catamenia (Amazon seems to have forgotten to stop disclosing these). The physical product mix hasn't got dramatically more expensive to send, then would it get dramatically more capex-intensive to warehouse? This is apparently not an exact proxy, but it seems unlikely.

So, though we tin can't be sure, information technology looks similar the capex is non going upwardly considering Amazon's existing business organization has become more than expensive to run, simply because Amazon is investing the growing pool of operation cash period into the future. All of this brings u.s. back to the start - Amazon's concern is delivering very rapid revenue growth merely not accumulating whatsoever surplus cash or profits, because every penny of cash is being ploughed back into expanding the business further. But, this is not because whatsoever given business runs permanently at a loss - it is because the profits from what is already in that location are spent on making new businesses. In the past, that was mostly in operations, but in recent years the investment firehose has over again been pointed at capex.

How long will this investment go along for? Well, do we believe that the conversion of products and businesses to online commerce is finished? Permit'southward rebase that revenue chart, and look at information technology as share of US retail revenue. Excluding gasoline, nutrient and things like timber and plants,all hard to ship, at least for now, Amazon has well-nigh 1%.

Overall, US commerce is growing very consistently:

And Amazon is taking an accelerating share of it.

Amazon has maybe i% of the US retail market by value. Should it end inbound new categories and markets and instead have profit, and by extension leave those segments and markets for other companies? Or should information technology proceed investing to sweep them into the platform? Jeff Bezos'southward view is pretty clear: proceed investing, because to accept profit out of the business organization would be to waste the opportunity. He seems very happy to keep seizing new opportunities, creating new businesses, and using every concluding penny to do it.

However, investors put their money into companies, Amazon and whatever other, with the expectation that at some point they will go greenbacks out. With Amazon, Bezos is deferring that profit-producing, investor-rewarding day almost indefinitely into the futurity. This prompts the proffer that Amazon is the world'southward biggest 'lifestyle business organization' - Bezos is running information technology for fun, not to evangelize economical returns to shareholders, at least not any fourth dimension soon.

But while he certainly does seem to be having fun, he is also edifice a visitor, with all the cash he tin get his hands on, to capture a larger and larger share of the time to come of commerce. When you buy Amazon stock (the chief currency with which Amazon employees are paid, incidentally), yous are buying a bet that he can convert a huge portion of all commerce to flow through the Amazon machine. The question to enquire isn't whether Amazon is some profitless ponzi scheme, merely whether you believe Bezos can capture the future. That, and how long are you lot willing to await?

January 2021

The essay above is now rather onetime, and amidst other things, it was written before Amazon started disclosing financials for AWS and for Market. I wrote most that here , and take written a few other things about Amazon also.

Source: https://www.ben-evans.com/benedictevans/2014/9/4/why-amazon-has-no-profits-and-why-it-works

0 Response to "Why I Will Never Do Business With Amazon Again"

Post a Comment